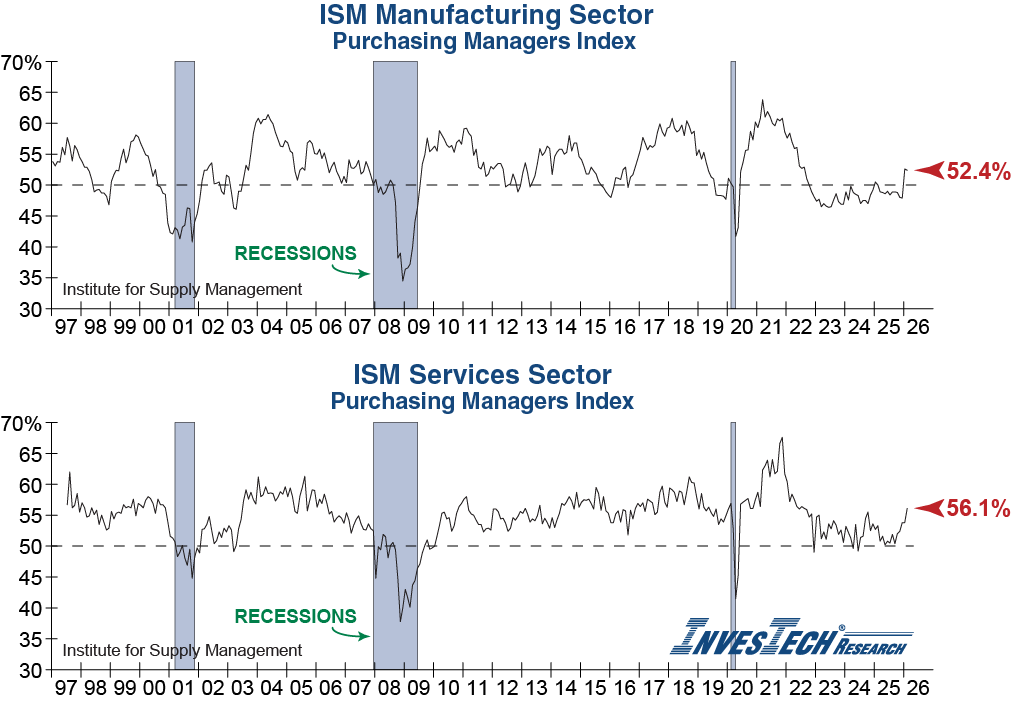

Earlier this week both the Institute for Supply Management (ISM) Manufacturing Purchasing Managers’ Index (PMI) and ISM Service PMI came in stronger than expected. The Manufacturing PMI ticked down slightly from 52.6% to 52.4%. Meanwhile, the Services PMI moved up from 53.8% to 56.1%.

Overall, with both Manufacturing and Services in expansion territory (>50%) these solid reports were positive signals for the direction of the economy. However, as tariff volatility continues, comments from the report indicate that buying activity could have been pulled forward in anticipation of higher costs later in the year. Additionally, the data for these reports was gathered prior to the escalation of the conflict in Iran, which began with strikes on February 28th.

Tariff uncertainty along with geopolitical instability could continue to make these key reports volatile. While the bounce was notable, we will be closely watching in the coming months as a continuation of the upward trend will be essential to confirm the recent positive developments. So only time will tell if this is the start of a new strong economic leg, or simply a mirage.