Today’s headlines are touting the strength of the labor market following the release of last month’s job numbers, yet there’s more to the story when you look under the surface. Employers added 315K jobs in August, which was better than economists’ expectations, but this was still the third lowest reading since the pandemic-induced recession. Additionally, the unemployment rate increased from 3.5% to 3.7%.

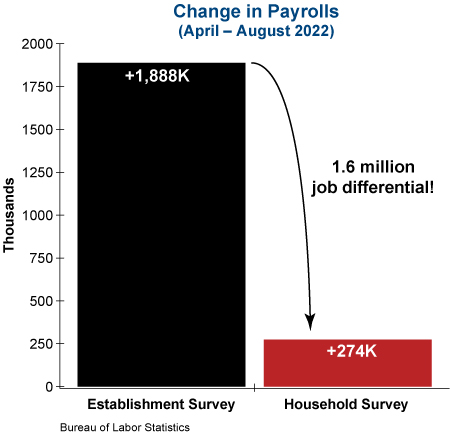

The figures above come from the Bureau of Labor Statistics’ (BLS) “Establishment Survey”, which surveys businesses and government agencies about their employment actions. The BLS also conducts a “Household Survey”, which surveys individual households about their employment situation. As shown in the graph below, there has been a difference of more than 1.6 million jobs between the Establishment Survey and the Household Survey in recent months! The difference becomes even more stark when it’s revealed that the entire gain in the Household Survey has been due to part-time employment, as full-time jobs have actually decreased over the past five months.

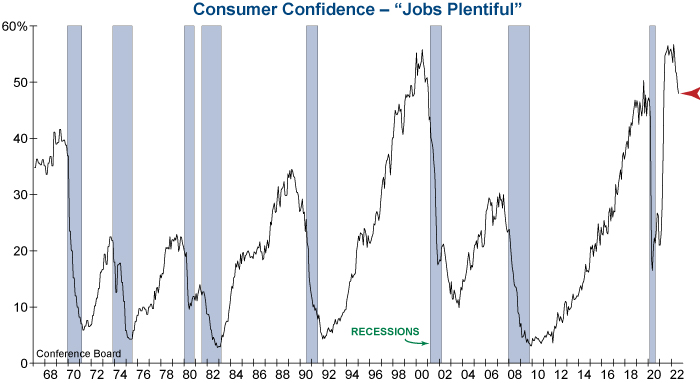

While the data above provides important context, these are still lagging indicators and don’t tend to predict where the labor market is headed. When we turn to a reliable leading employment indicator –the share of consumers that see jobs as being “plentiful”– the situation looks even worse. As shown below, this measure continued to decline in Tuesday’s release and is now down by over -8 points from its March peak. Every other time this indicator has fallen by a similar amount in the past, the economy was destined for recession.

So, while the labor market remains strong enough to keep the Federal Reserve on a tightening course, the worsening employment trend poses a major threat to the U.S. economy going forward.

Eli Petropoulos, CFA – Sr. Market Analyst