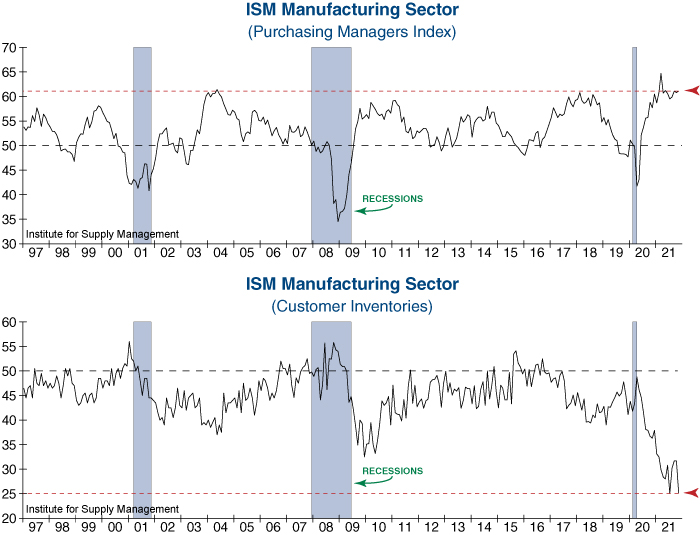

The ISM Manufacturing Index ticked higher to a reading of 61.1 in November, keeping it at a historically strong reading. Manufacturers continue to see robust demand with new orders continuing to grow, which is helping to offset challenges presented by inflation, a shortage of qualified labor, and supply-chain issues for the time being. As stated by the Institute for Supply Management, “Coronavirus pandemic-related global issues — worker absenteeism, short-term shutdowns due to parts shortages, difficulties in filling open positions and overseas supply chain problems — continue to limit manufacturing growth potential.” As a result, the Customer Inventories component sunk back to its lowest level on record last month in a clear sign that supply-demand imbalances are persisting.

While the manufacturing sector remains on strong footing, we will be watching this leading indicator closely for signs of slowing demand and changes in the global supply chain bottlenecks. Additionally –as published in the November issue of InvesTech Research– it is worth noting that equity market returns tend to be underwhelming following extremely high readings (> 60) in the ISM Manufacturing Index.