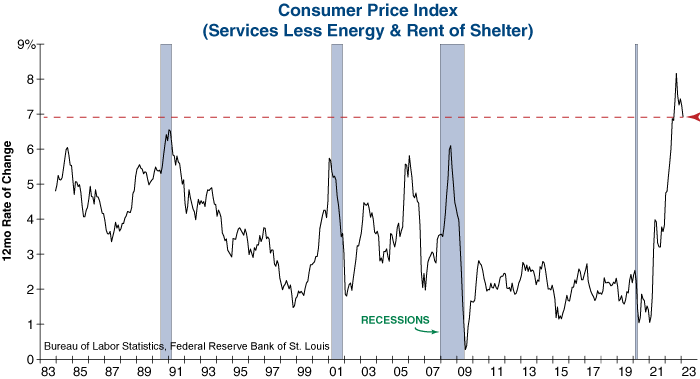

Yesterday’s Consumer Price Index (CPI) report showed that inflation slowed from 6.4% to 6.0% on an annual basis in February, however the report also made it clear that sticky inflation remains an issue. Most notably, services inflation excluding energy and housing prices remains at one of the highest readings in its 40-year history. This inflation measure was referred to as one of the “most important” data points to watch by Fed Chair Jerome Powell, as it tracks how embedded inflation is becoming in the economy. Simply put, this inflation tool shows the impact that wage growth has on prices. The stronger and more persistent wage growth becomes, the greater the risk of a wage-price spiral developing – something the Federal Reserve wants to avoid at all costs.

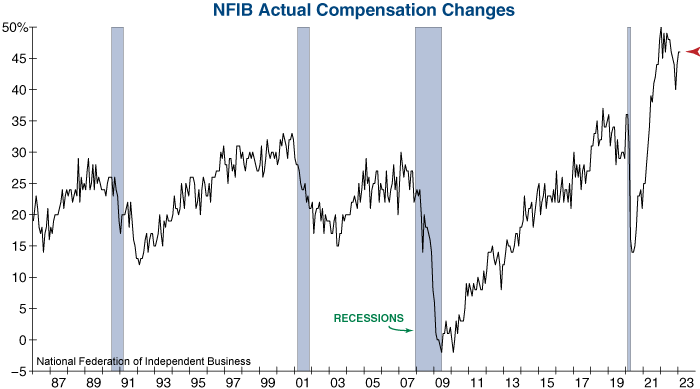

Unfortunately for the Fed, small businesses are reporting that wage growth remains robust. According to the latest survey from the National Federation of Independent Business (NFIB), 46% of small businesses reported raising compensation within the last three months, one of its highest readings since the data series’ inception in 1986. So, while there are early signs that the labor market has started to cool, it has not yet shown through in wages.

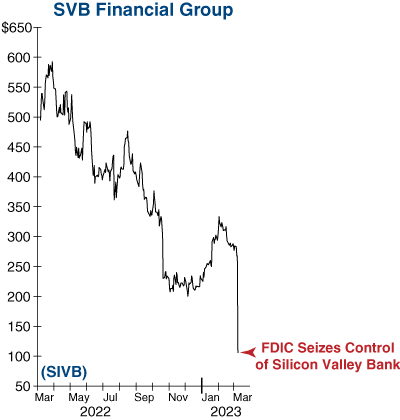

Persistent inflationary pressures and wage growth are clearly compelling the Federal Reserve to continue hiking interest rates, but the recent failures of Silicon Valley Bank and Signature Bank could cause central bankers to temporarily stand pat at next week’s FOMC meeting.

Regulators took control of Silicon Valley Bank on Friday followed by Signature Bank over the weekend, as neither was able to adequately cover the flood of withdrawals they received last week. While both are regional banks, their collapses are still the second and third largest bank failures in U.S. history – exceeded only by the failure of Washington Mutual in 2008.

Confidence in the banking system has seemingly been restored after the Federal Reserve, Treasury Department, and Federal Deposit Insurance Corporation (FDIC) jointly announced that they would guarantee all deposits in both failed banks. They also announced they would provide additional funding to help assure other banks have the ability to meet the needs of all their depositors. Yet, we have to wonder if larger risks still lie beneath the surface.

As the March FOMC meeting approaches, the Fed is stuck between a rock and a hard place with no good answer as it attempts to bring inflation down to its 2% target rate while also ensuring stability of the financial system.

Eli Petropoulos, CFA – Sr. Market Analyst