Weekly Hotline: April 3, 2026

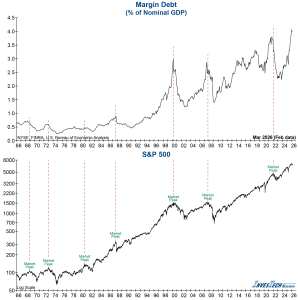

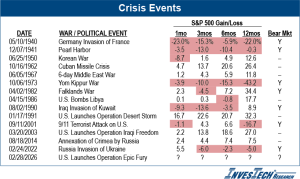

This week marked the end of a turbulent first quarter of 2026, and markets briefly rallied as investors navigated headline driven volatility. Key proprietary technical indicators, however, warn that the risk is far from over.

MACROECONOMIC UPDATE

- Consumer Confidence was relatively unchanged in March as it ticked up from 91.0 to 91.8. While consumers felt better about the Present Situation (rising 4.6 points to 123.3), their Future Expectations fell 1.7 points to 70.9. Also, Inflation Expectations rebounded sharply to the highest level since August 2025.

- The Institute for Supply Management (ISM) Manufacturing Report showed continued expansion (>50%) as the overall gauge ticked up from 52.4% to 52.7%. However, the Prices component rose dramatically from 70.5% to 78.3% as price pressures increased to the highest level since 2022. This is a worrisome development for inflation – especially as consumers are already stretched thin.

- The Jobs Report for March showed a positive turnaround from February as 178,000 jobs were added and the Unemployment Rate dipped from 4.4% to 4.3%. While this is an improvement, the last two months showed significant revisions and reveals the volatility of this monthly figure.

- All in all, these developments could effectively take a Fed rate cut off the table in the coming months as the FOMC is forced to turn their focus to inflation.

TECHNICAL UPDATE

- InvesTech’s Artificial Intelligence and Gorilla Indexes bounced this week, as would be expected in a rally, but remain well below their highs of late last year. A renewed decline in these critical indicators and a break through Monday’s lows would likely confirm a bear market ahead.

- Bearish Distribution in the InvesTech Negative Leadership Composite (NLC) dropped further this week to -39. An accelerated decline to -100 would confirm the probability that a bear market is in control.

INVESTECH MODEL FUND PORTFOLIO

There are no changes to the Model Fund Portfolio this week, which is comprised of 58% long positions, 7% in an inverse index ETF, 5% in an intermediate Treasury ETF, and 30% cash held in short-term Treasurys or a money market fund. This results in 51% net equity exposure.